Investors focusing on climate change face a central paradox.

On the one hand, excitement around the energy transition is skyrocketing. Over $70 trillion in global capital is aligned with the transition to net-zero by 2050, a sevenfold increase since the 2015 Paris Accords.

Despite this, the world’s dependence on fossil fuels hasn’t waned. Demand for coal, gas, and oil hit record highs in 2022. From 2000 to 2022, the world only achieved a 4% reduction in carbon dependency, with fossil fuels supplying 82% of primary energy.

Our sluggish energy transition raises a pivotal question: how must global capital allocation toward climate change evolve?

We believe the ‘Investor Overton Window’ on climate change must expand significantly in the near future, as the need for more immediate climate action grows.

Here, we outline ten predictions for investors as short- to medium-term decarbonization expectations shift.

- Climate Adaptation Takes Center Stage

- Carbon Removal Becomes a Multibillion Dollar Industry

- Geoengineering Becomes Mainstream

- Carbon Prices Rapidly Expand

- The US Energy Transition Receives Bipartisan Support

- Solar & Wind Continue Along S-Curve Growth

- Greater Importance Is Given to Breakthrough Tech

- There Is a Global 'Marshall Plan' for Grids

- China & India Go from Laggards to Leaders

- GDP Ceases to Be a Universal Measure of National Progress

(1) Climate Adaptation Takes Center Stage

Mitigation efforts have attracted investment for more than a decade. Now, attention is shifting towards climate adaptation, with growing bipartisan support in the US.

The Biden Administration released climate adaptation and resilience plans across 23 agencies of the federal government. Meanwhile, House Republicans are strategizing to “protect American lives and livelihoods by deploying smart resilience and mitigation investments in conservation and adaptation solutions.”

What characterizes our new focus on climate adaptation?

Emerging Research

The Global Commission on Adaptation Report highlights eight key areas for climate adaptation investment: (1) Early Warning Systems, (2) Climate Resilient Infrastructure, (3) Dryland Agricultural Crop Production, (4) Mangrove Protection, (5) Water Infrastructure, Destination, and More, (6) Insurance and Reinsurance, (7) Heat Stress, (8) Urban Planning and Adaptation.

Infrastructure Investments

A $53 billion proposal from the US Army Corps of Engineers aims to bolster coastal ecosystem resilience by building breakwaters, seawalls, and levees. This infrastructure overhaul could significantly reduce future flood risks and economic costs related to storm events.

Insurance Concerns

The US has sustained 363 weather and climate disasters since 1980, totaling over $2.59 trillion in damages. These events are leading some private insurers to retreat from high-risk areas. State Farm and Allstate confirmed they would stop issuing new home insurance policies in California, and Farmers and AAA have ended many homeowner insurance policies in Florida. This retreat by private insurers places even more pressure on the federal government to provide relief.

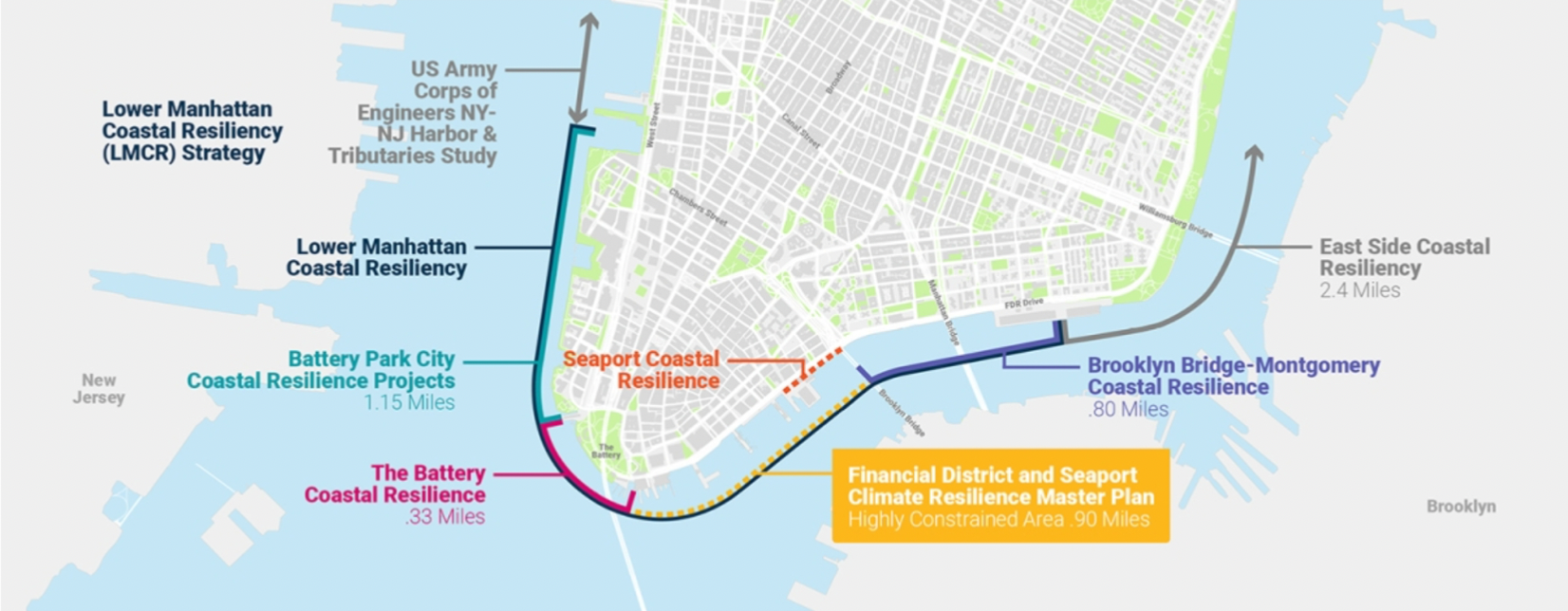

Exhibit 1 - Major metropolitan areas, including NYC, are developing adaptation strategies.

Source: Lower Manhattan Climate Resilience Study, NYC Economic Development Corporation

(2) Carbon Removal Becomes a Multibillion Dollar Industry

The carbon removal industry is quickly growing. The International Panel on Climate Change (IPCC) says carbon dioxide removal (CDR) is required to achieve global net-zero carbon and greenhouse gas emission goals.

Here’s how the industry is gaining momentum:

Government Support

The US Bipartisan Infrastructure Law earmarked $3.5 billion for the establishment of four direct air capture hubs. The Department of Energy allocated an additional $1.2 billion for projects like Battelle, Climeworks, and others, set to create thousands of jobs while removing 2 million metric tons of CO2 from the atmosphere annually.

These investments reflect a robust and growing governmental commitment to advancing carbon removal initiatives.

Global Competition

Elon Musk’s foundation funded a $100 million competition, XPRIZE Carbon Removal, that invites companies around the world to create and demonstrate CDR solutions.

Teams must demonstrate a working solution at a scale of at least 1,000 tons removed per year, model their costs at a scale of 1 million tons per year, and show a pathway to achieving a scale of gigatons per year in the future.

Corporate Commitment

Frontier Climate’s ambitious initiative, backed by tech industry giants including Stripe and Alphabet, pledges to purchase over $1 billion in permanent carbon removal between 2022 and 2030. Across the market, there is a growing acceptance of CDR technologies' impact, and private enterprises are working hard to overcome roadblocks to scalability.

Exhibit 2 - Net zero scenarios in modeling, by both the IEA and IPCC, rely significantly on carbon removal.

Source: Jefferies, IEA

(3) Geoengineering Becomes Mainstream

Geoengineering, once a scientific taboo, is now gaining traction globally. Both governments and private companies are exploring it as a viable route for climate intervention.

US Government Initiatives

The 2022 federal Appropriations Act, signed by President Biden, directs his Office of Science and Technology Policy to develop a cross-agency group to coordinate research on solar geoengineering. This group will coordinate with NASA, the National Oceanic and Atmospheric Administration (NOAA), and the Department of Energy.

European Commission’s Stand

The European Commission is calling for international talks on the potential dangers and governance of geoengineering, saying such interventions pose ‘unacceptable’ risks. The EU maintains a stance against developing or testing solar radiation modification, but it will fund two projects to assess such techniques.

China’s Program

In 2020, China announced plans to significantly expand an experimental weather modification program. The ambitious project aims to cover an area of over 5.5 million square kilometers.

Private Sector Involvement

Companies are also showing interest in geoengineering. Make Sunsets, backed by venture capitalist Tim Draper, is one such example. The company aims to send balloons filled with sulfuric dioxide into the atmosphere, in order to cool the planet and combat climate change.

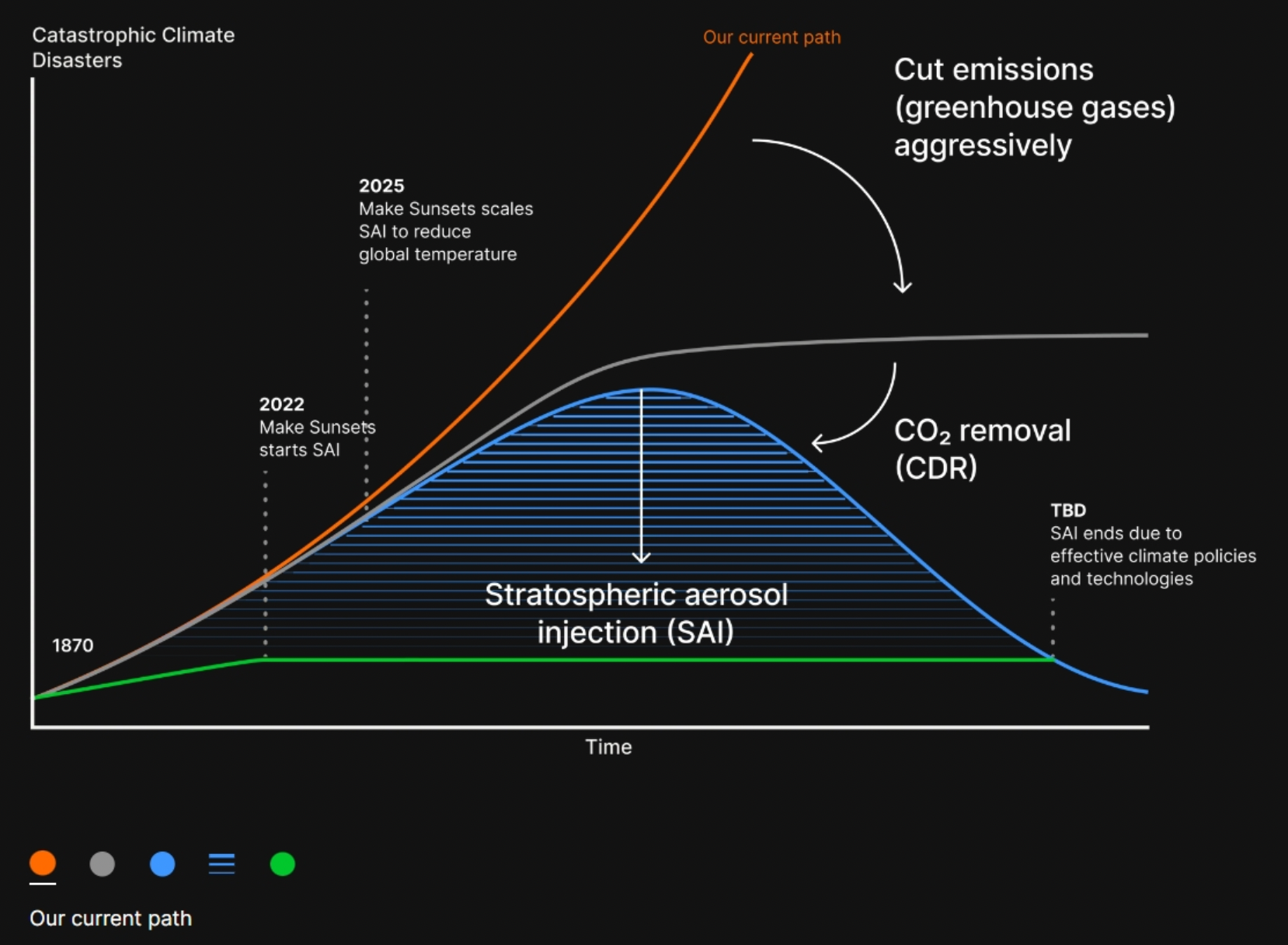

Exhibit 3 - Stratospheric Aerosol Injection: an effective solution to buy time for other efforts to take hold.

Source: Make Sunsets

(4) Carbon Prices Rapidly Expand

The IPCC has expressed high confidence that the price of carbon increases significantly if a higher level of stringency is pursued. There’s a substantial variation in carbon prices across different models and scenarios.

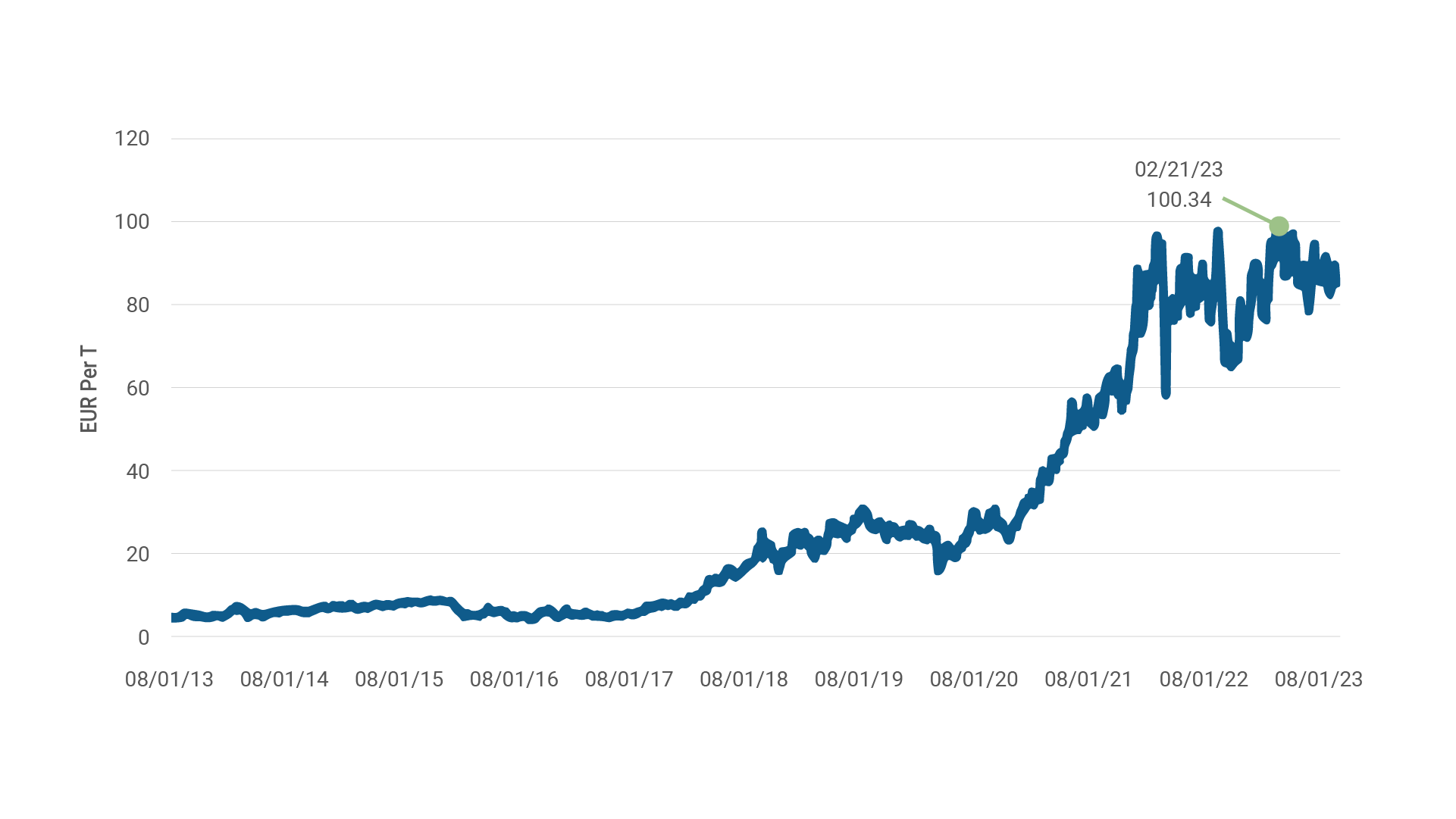

The carbon market price in the EU’s ETS was 4.33 EUR/t in 2013. By August 29, 2023, it soared to 85.68 EUR/t. Within this period, the peak was 100.34 EUR/t on February 21, 2023.

Comparatively, the UK's ETS was trading at 48.03 GBP/t on August 29, 2023.

we could point to needing a c.2.5x increase in carbon prices to achieve many goals they

It’s crucial to note that even these elevated prices, among the world’s highest, are still insufficient for meeting the 2030 and 2050 climate goals. Nonetheless, they demonstrate that economies can withstand high carbon prices.

These price movements are a positive indicator, pointing toward a growing global commitment to more stringent climate mitigation measures.

Exhibit 4 - EU ETS Carbon Market Price (8/1/13 - 8/9/23)

Source: FactSet, Jefferies

(5) The US Energy Transition Receives Bipartisan Support

Despite the political noise around ESG, the US energy debate is evolving. A bipartisan consensus is emerging around the energy transition, driving policies that lay the groundwork for a net-zero America.

Recent legislation includes:

Inflation Reduction Act (IRA)

The most significant bill to date. One year into the IRA, $278 billion has been announced for clean energy investment, resulting in 272 new projects and the potential creation of 170,000 new jobs as reported by the Rocky Mountain Institute.

Farm Bill

A forthcoming $1.5 trillion Farm Bill could also significantly impact agriculture and food systems, further showcasing bipartisan support for a cleaner and more sustainable future.

Bipartisan Infrastructure Bill and CHIPS Act

Both pieces of legislation include investments in decarbonization.

The Bipartisan Infrastructure Bill allocates $7.5 billion towards a national network of 500,000 electric vehicle chargers; $50 billion to project against droughts, floods, and wildfires; $65 billion for clean energy and grid-related investments; $55 billion to expand access to clean drinking water; and $21 billion to clean up Superfund and brownfield sites and cap orphaned oil and gas wells.

The CHIPS Act is estimated to direct $67 billion toward the growth of zero-carbon industries.

Additional Efforts from the Biden Administration

An additional $12 billion has been made available to automakers and suppliers for expanding plants to produce electric and other advanced vehicles. The initiative has not faced Republican opposition.

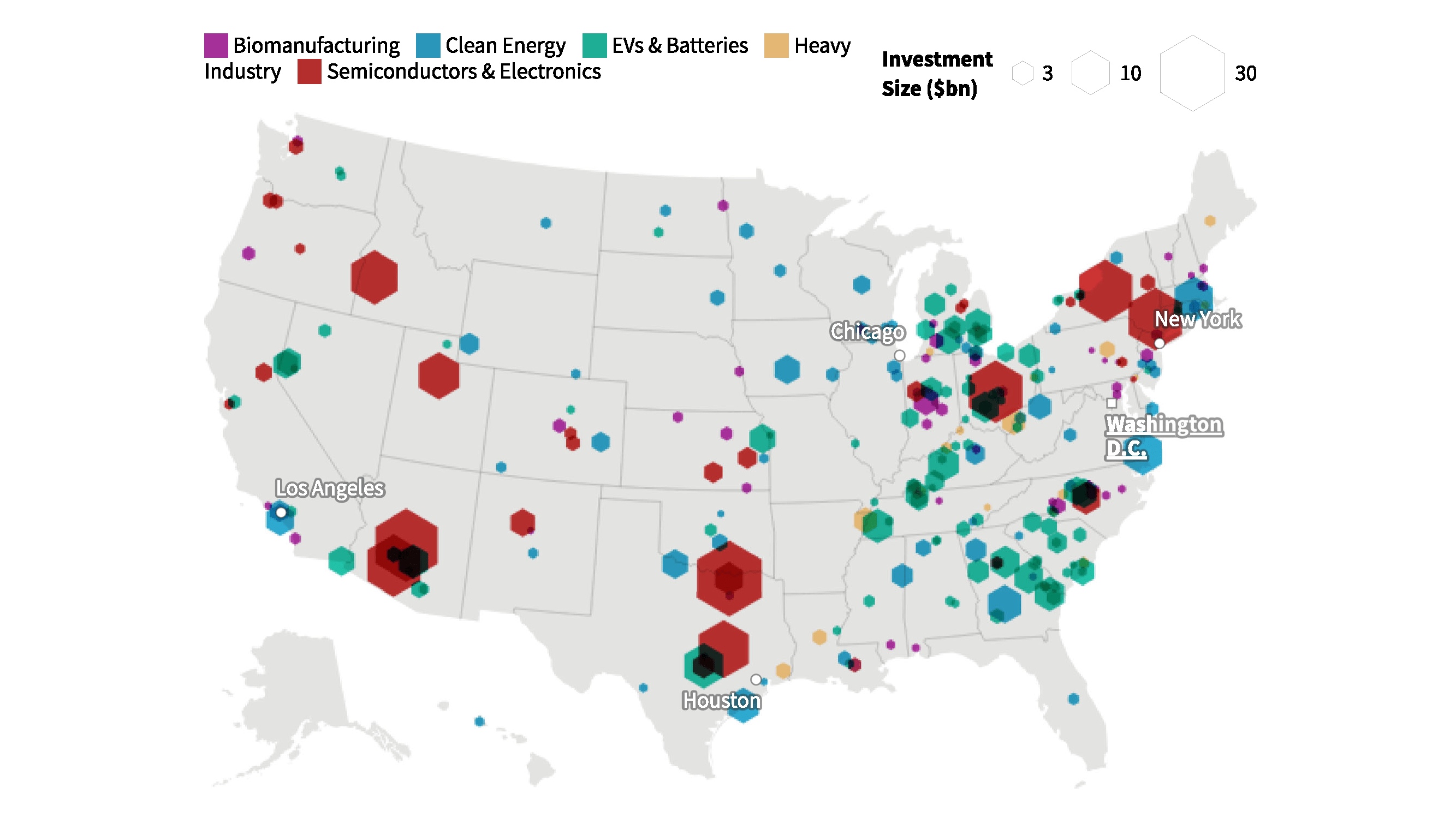

Exhibit 5 - Clean energy investments post policy announcements since 2021.

Source: RMI, White House

(6) Solar & Wind Continue Along S-Curve Growth

Over the last decade, advancements in solar, wind, and electric vehicle battery technologies have vastly outperformed prior assumptions around market penetration.

The costs for these renewable technologies have followed a consistent downward trajectory, allowing them to become more accessible and efficient over time. The solutions have followed a promising S-curve of growth and adoption.

This cost reduction, paired with significant technological enhancements, paved the way for record deployments of solutions once considered niche and uncommercial by investors. Contrary to the expectations of many, these solutions have transcended the barriers that often lead to linear adoption and slow growth.

Looking ahead to 2030, we expect continued exponential growth for these established renewable energy solutions. Continued policy support, various industrial policies, and ongoing technological breakthroughs will all contribute to additional growth, with numerous opportunities for investors.

Exhibit 6 - Global solar PV capacity is set to almost 3x between 2022-2027, showing clear s-curve characteristics.

Source: IRENA, Jefferies

(7) Greater Importance Is Given to Breakthrough Tech

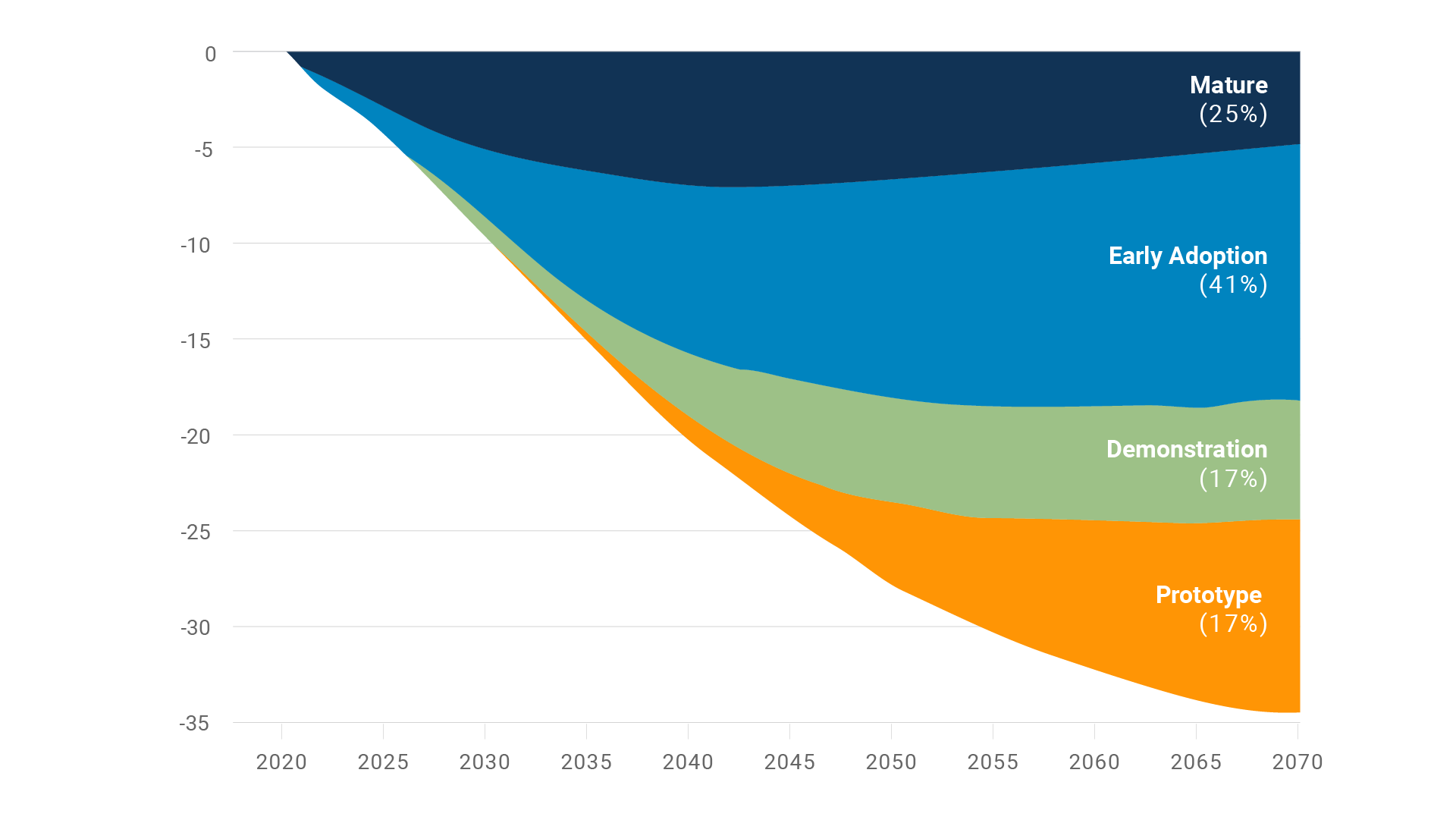

The International Energy Agency (IEA) reports that over 75% of the cumulative emissions reductions needed for its 2050 net-zero scenario are not yet commercially available. In fact, 35% are still in the prototype or demonstration phase.

Advancements in renewables, enhanced battery range, and energy efficiency have successfully reduced emissions in sectors like road generation and power generation – but significant emission reductions are still needed in more difficult sectors. These include shipping, trucks, cement, and steel, which require the use of technologies not currently available at scale.

It is clear that without a major acceleration in breakthrough solutions, decarbonization targets will not be achieved.

We believe investors should direct capital towards seemingly unrealistic solutions today, such as nuclear fusion and small modular reactors. Some of these have the potential to be part of the range of options available through 2050.

This proactive approach will allow investors to make informed predictions about which technologies are likely to become commercial and within what timeframe, thus supporting the push toward global decarbonization targets. A focus on these areas would also improve underlying technologies, reduce costs, and accelerate deployment.

Exhibit 7 - 75% of the emissions reductions required in a net-zero scneario are from technologies that are not commercial today.

Source: IEA, Jefferies

(8) There Is A Global ‘Marshall Plan’ for Grids

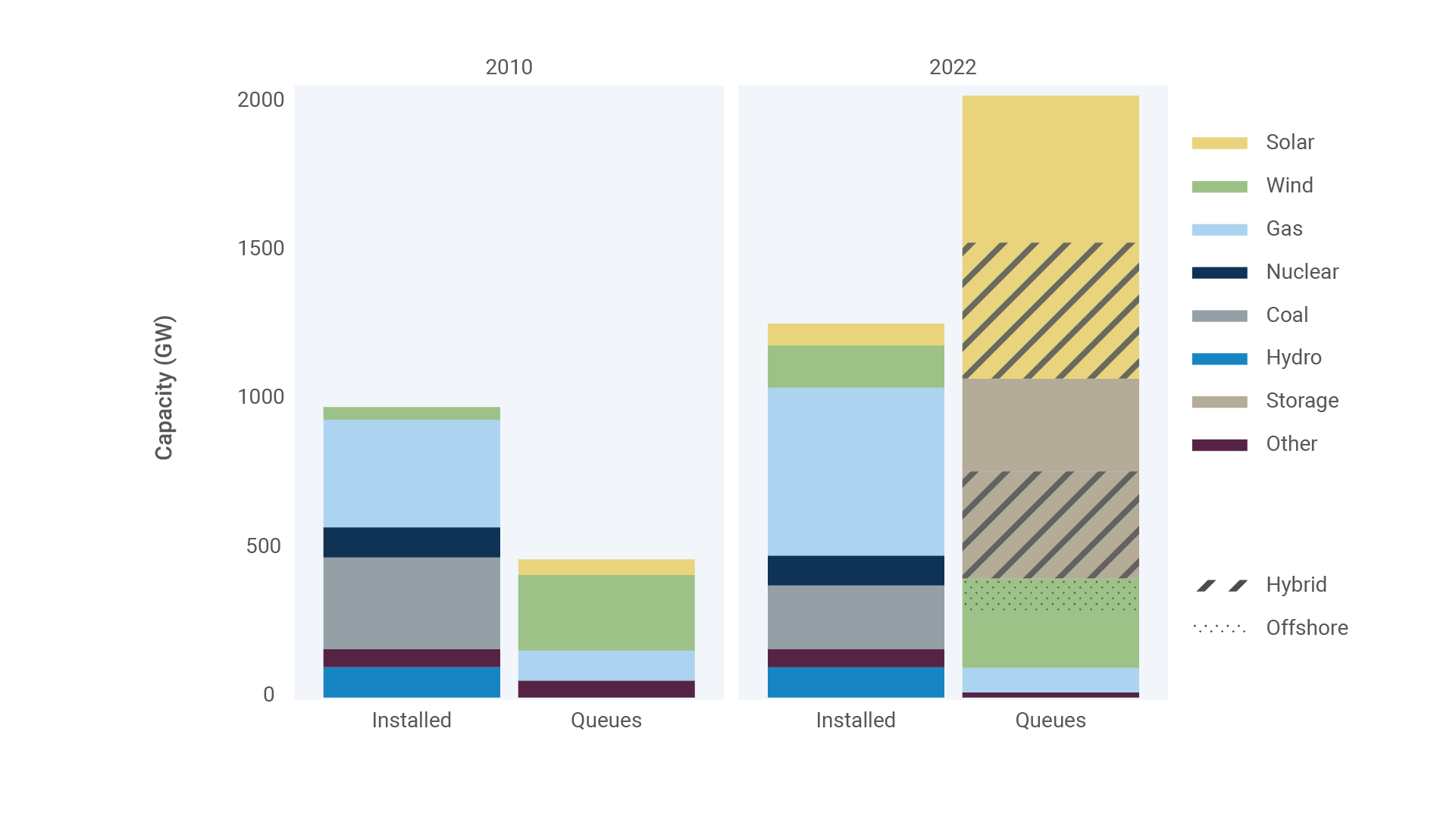

The importance of power grids in the decarbonization of the energy system is becoming increasingly apparent. Electricity accounts for approximately 20% of final energy consumption globally. As more end-users, such as electric vehicles and buildings, opt for electrification, the demand for power is predicted to more than double in the US and Europe. This surge will significantly burden the existing grid infrastructure.

Challenges to overcome include:

Lead Times for New Transmission Lines

In the US, over 10,000 projects (around 1,400 GW) of generation capacity and 680 GW of storage await interconnection. In the UK, over 600 transmission projects are waiting for grid connection, with some delayed for up to 13 years.

Reasons for delays include complex permitting processes, involvement from multiple stakeholders, and technical challenges.

Grid Capacity

Grid capacity constraints are a major obstacle to enhancing power grids. Issues like limitations in authorized transmission capacity, transmission outages, and load variations are pressing concerns.

Flexibility

Modern grids must offer solid flexible generation as clean energy sources integrate. Today's fossil sources, such as gas peaker plants, provide this flexibility. Grids of tomorrow will need to combine storage and smart demand response systems to maintain flexibility.

Regional Interconnections

Improving cross-border electricity interconnections is crucial for decarbonizing power systems.

The UK currently depends on about 8GW of interconnected power from mainland Europe. This interconnection needs to improve in both the UK and Europe. In the US, the lack of a unified power grid or federal authority for infrastructure approval is a significant hurdle.

Addressing these challenges head-on is vital for upgrading the grid infrastructure in the developed world to meet growing demand and support the global decarbonization effort.

Exhibit 8 - The total generation and storage capacity in active queues in the US has grown 4x in the last decade.

Source: Lawrence Berkeley National Lab, Jefferies

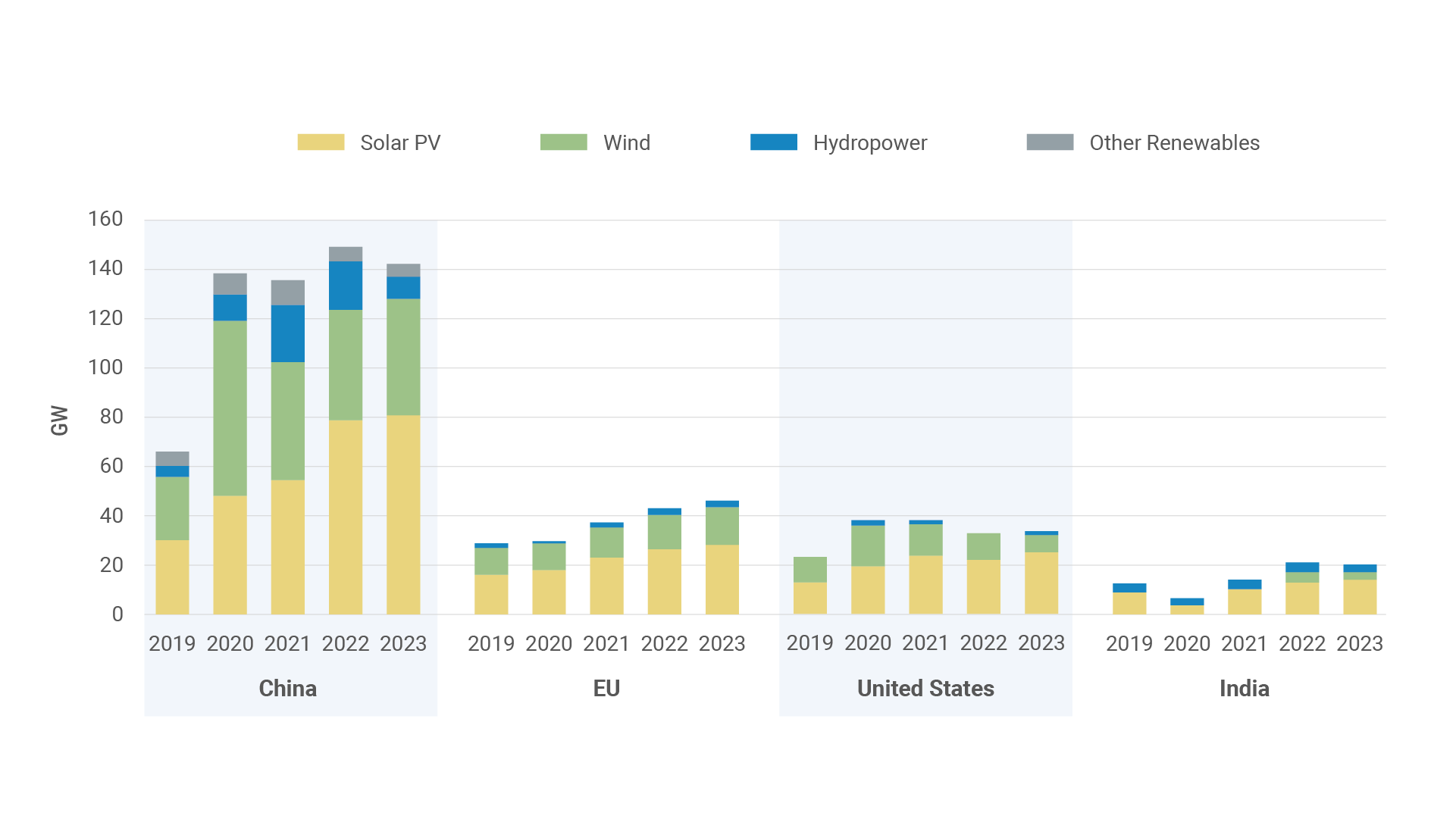

(9) China & India Go From Laggards to Leaders

There is a growing global consensus that the key to a net zero world resides in decisions made by emerging economies. All projected growth in energy demand over the next 25 years is concentrated in these countries. Among them, China and India play especially critical roles.

China’s Role

China is facing a unique energy duality. It is both the leader in carbon emissions and renewable energy development.

Despite accounting for a third of global CO2 emissions, China is the world’s leading producer of wind and solar power, ranking first in intellectual property and competitiveness in offshore wind power and advanced solar technology for the past decade.

Since 2015, China’s spending on low-carbon research and development has surged by 70%, per the IEA. The nation recently pledged to peak its CO2 emissions before 2030 and achieve carbon neutrality by 2060. No national pledge is as significant as China’s. Early indicators suggest the country is on track to achieve its first goal before 2030.

While China deserves recognition for these efforts, its coal expenditure continues to run rampant. The country’s pace of approval for new coal plants doubled to its highest levels in 2016 according to BloombergNEF data, countering its clean energy strides.

India’s Role

In contrast, India’s per capita energy use and emissions are below half the global average. The country's renewable energy expansion is propelled by solar energy, with a fivefold increase in installed solar power over the past decade. India's share of the global solar market is anticipated to jump from under 10% to around 30% by 2040.

India’s coal consumption remains high, comprising 55% of its energy needs, but the nation’s clean energy efforts go beyond solar. As the 4th largest listed equity market globally, India’s emerging status as a hub for low carbon investment cannot be overlooked.

Exhibit 9 - Renewable capacity additions in China, the EU, the US, and India (2019 - 2023).

Source: IEA

(10) GDP Ceases to Be A Universal Measure of Wealth

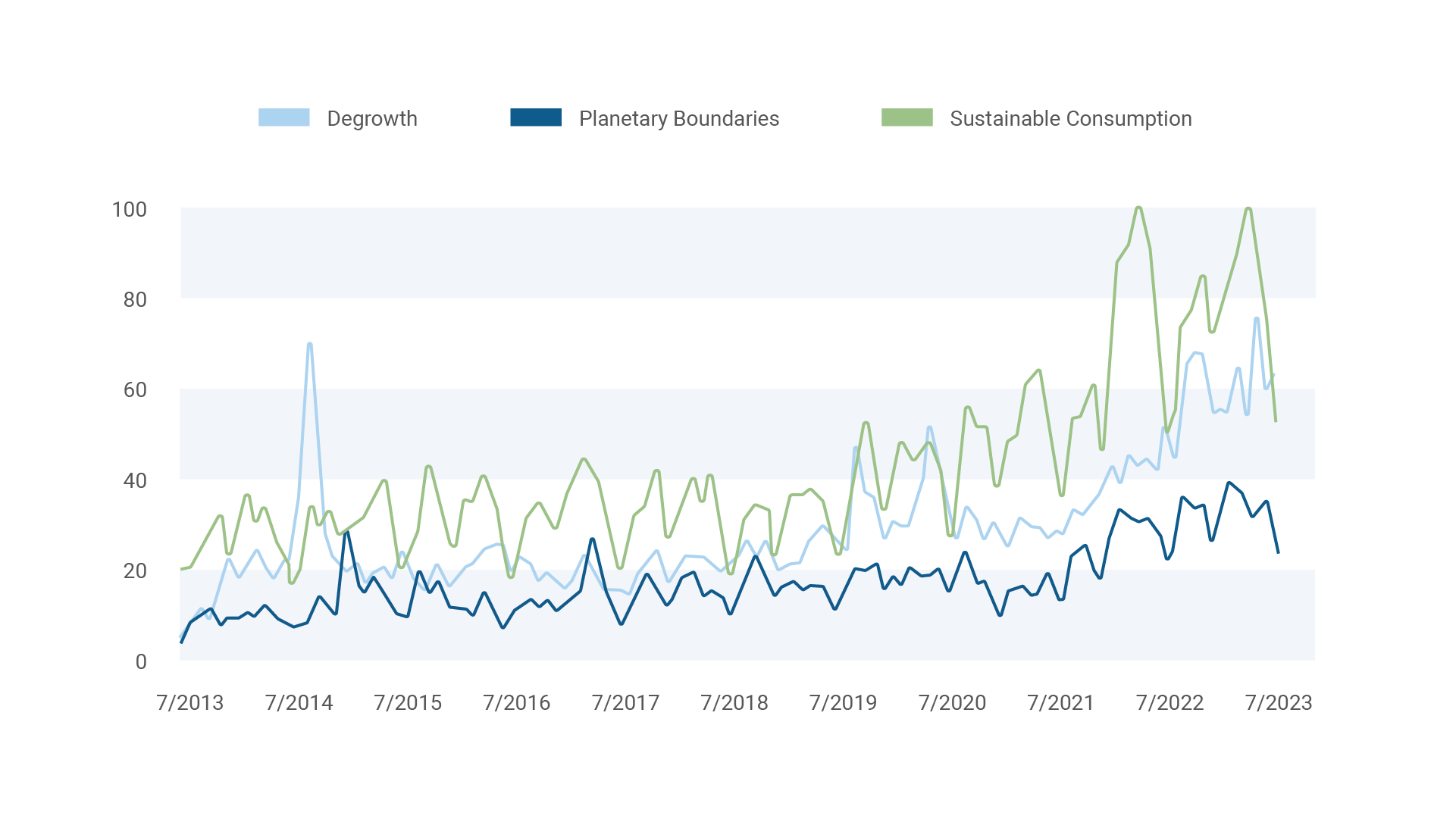

The notion of a ‘post-growth’ economic mindset is beginning to enter mainstream discourse. Degrowth can be defined as an ‘equitable downscaling of production and consumption that increases human wellbeing and enhances environmental conditions’.

Degrowth in Business

In a business context, degrowth involves a systemic restructuring. It means turning away from excess production and consumption and concentrating on meeting universal basic needs within local bio-capacities. Surpluses would be invested in common goods and services.

In a degrowth scenario, the global economy would not experience universal degrowth but aggregate degrowth, acknowledging varied needs across different regions.

Beyond GDP

The movement also advocates for metrics beyond GDP, as it is poorly equipped to assess a nation's well-being and sustainable development effectively. Governments worldwide are working on new metrics to report alongside GDP, focusing on a balance between economic growth, well-being, and sustainable development.

Support from IPCC

The IPCC's Working Group III report for the first time discussed the need for degrowth-related steps given increased awareness and discussion around resource constraints related to the energy transition.

The authors write, "Demand-side measures and new ways of end-use service provision can reduce global GHG emissions in end-use sectors by 40–70% by 2050 compared to baseline scenarios, while some regions and socioeconomic groups require additional energy and resources. Demand-side mitigation response options are consistent with improving basic well-being for all (high confidence)."

Broader society is becoming attuned to these themes, with Google searches having increased over the past decade.

Increasing Acceptance and Regulation:

While there are no explicit ‘degrowth’ funds, the rise in circular economy fund launches post-COVID, from three to eleven, indicates growing interest.

European regulations further support this trend, with the circular economy being a key objective in the EU Taxonomy. The European Parliament's "Beyond Growth" conference earlier this year emphasized the implementation of a post-growth, future-fit EU, highlighting the increasing acceptance of degrowth-related ideas.

The shift toward a post-growth economy underscores the world’s concerted move towards sustainable development. In coming years, we anticipate a rise in demand for solutions addressing these themes, met by an increase in products catering to this new economic approach.

Exhibit 10 - Global Google search trends (7/1/13 - 7/31/23).

Source: Google Trends, Jefferies